Cashback Was the Wrong Reward

Tuyo's "Buy Now, Pay Maybe" is a useful doorway into a larger question: what should the reward layer recognise when claims are cheap and behavioural proof starts to matter?

The card that might not charge you

A card that might not charge you is a strange object.

That is the hook behind Tuyo's "Buy Now, Pay Maybe" campaign. The mechanic is simple: tap the card, make the purchase, and maybe Tuyo pays for it. The user walks away with the item, while the card moment still feels like normal payment.

But something else has been added.

Suspense.

That is what makes the campaign useful. Not because random reimbursement is the future of finance. It probably is not. It is useful because it points at something the rest of the category has been slow to make interesting.

The reward layer is waking up, and it may not look like just cashback.

Spend was always a thin signal

For most of its life, consumer finance has treated rewards as an accounting problem. Spend this much, get this many points. Use this card, get this percentage back. Hit this tier, unlock this voucher. The user spends. The program rebates. The bank calls it loyalty.

But loyalty was never the right word. Most reward programs do not recognise loyalty. They recognise spend.

Spend is easy to count. It is also a thin signal.

The person who spent 500 dollars at a brand last week may be less loyal than the person who has returned every month for five years. The person who bought the most expensive ticket may be less valuable to a community than the person who showed up quietly every Tuesday for two winters. The person who qualifies for the cashback may not be the person a merchant actually wants in the room.

The person you want in the room is usually the person who comes back.

They might bring friends. They might become the first hundred regulars. They might make the place feel alive before the paid ads start working. There is little better marketing than a good experience moving through people who already care.

That is the gap the next reward layer has to close.

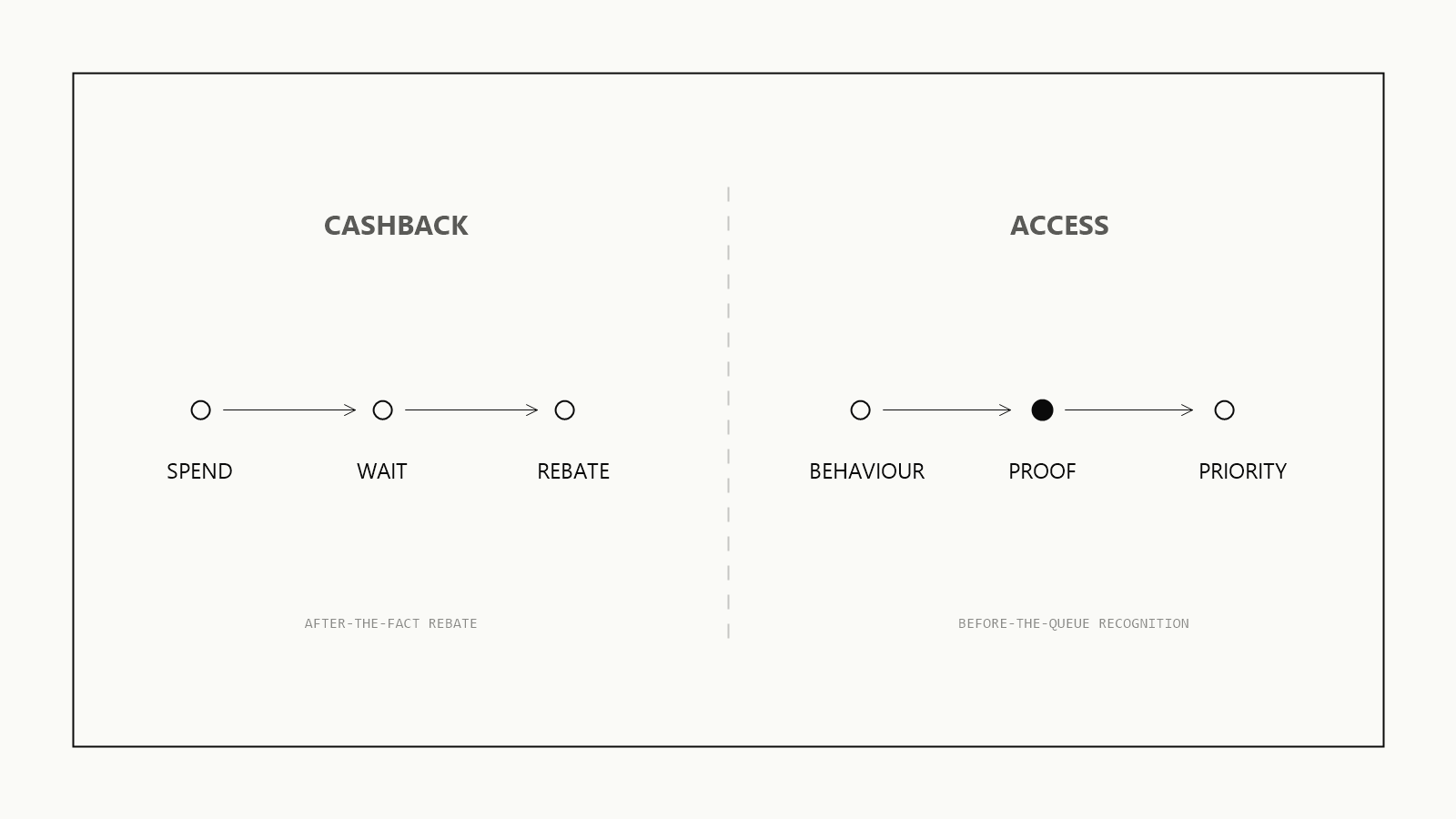

The old system asks: how much did you spend?

Tuyo asks: what if this transaction became exciting?

The better system asks: what has this person actually done often enough, long enough, and recently enough to deserve access before everyone else?

That is the shift. Cashback pays you after the fact. Access recognises what the fact means.

The false futures: accounting or casino

The false futures are easy to see.

One version is accounting with better colours. Points, cashback, vouchers, tiers, balances, partner catalogues, expiry dates. A user becomes a coupon accountant. How many points do I have? When do they expire? What can I redeem? Why is the thing I earned less useful than the thing I paid for?

The other version is the casino. From a product-design point of view, randomness creates attention. The payment moment becomes a scratch card. Every tap carries the possibility of a small escape from the price.

You can see why that works.

You can also see why it is incomplete.

Randomness can buy attention. It does not tell the merchant who should be reached. It does not tell the user what they earned and why. It turns a transaction into a maybe.

And maybe is only a mechanic.

But mechanics matter because they reveal where the next product can be built.

The reward layer becomes behavioural

The stronger version of the reward layer is behavioural. The best version is proof.

Banks, card networks, and neobanks already sit close to one of the richest payment-history datasets in consumer life. They can observe or infer where people spend, how often, at what time, and with what recurring financial patterns around it. They can see the Tuesday coffee. They can see the independent restaurants that keep getting chosen over chains. They can see recurring payments people forget. They can see which merchants earn a return visit and which ones only win once.

The user knows much of this too, in a lived way. The problem is that most of the signal evaporates.

It becomes a line item. A push notification. A monthly spending category. Maybe an insultingly bad offer for a cafe in a city the user does not live in.

The data exists. The intelligence layer is still thin, fragmented, and often badly routed. Where it does exist, it rarely creates clear value for the user, the merchant, and the platform at the same time.

That layer is valuable to the user, the merchant, and the platform. For the user, it can turn history into access. For the merchant, it can turn broad promotion into precise routing. For the platform, it can turn a static transaction record into a permissioned map of who should be offered what, when, and why.

Good businesses already understand the emotional version of this. Starbucks putting your name on a cup was not deep technology. But it was better than treating everyone as another double shot americano moving through the line. The point was the feeling that the system saw you and made a connection beyond the sale.

Amex understands the premium version. Its power is not that people love annual fees. It is that the fee turns into access: lounges, reservations, events, upgrades, priority. The product is not a rebate. It is a better place in the queue.

Eugene Wei's Status as a Service is useful here because good status systems are not just piles of perks. They are social positions that feel earned. The visible reward matters because there is some proof of work underneath it.

That is what most loyalty programs copied badly. They copied the surface: tiers, badges, balances, catalogues. They missed the mechanism.

The best reward is the one that does not feel like redemption.

It feels like the system understood why you belonged there.

The primitive is the receipt

This is where Tuyo is more interesting as a symptom than as a product. "Buy Now, Pay Maybe" notices that the payment moment can carry emotion. It notices that finance does not have to be beige utility software. It notices that rewards can sit at the moment of action, not three statements later.

But it still leaves the primitive unresolved.

The primitive is the receipt.

Not the receipt as a PDF in your email. The receipt as proof that a specific behaviour happened, from a specific source, across a specific window, without exposing the whole archive underneath it.

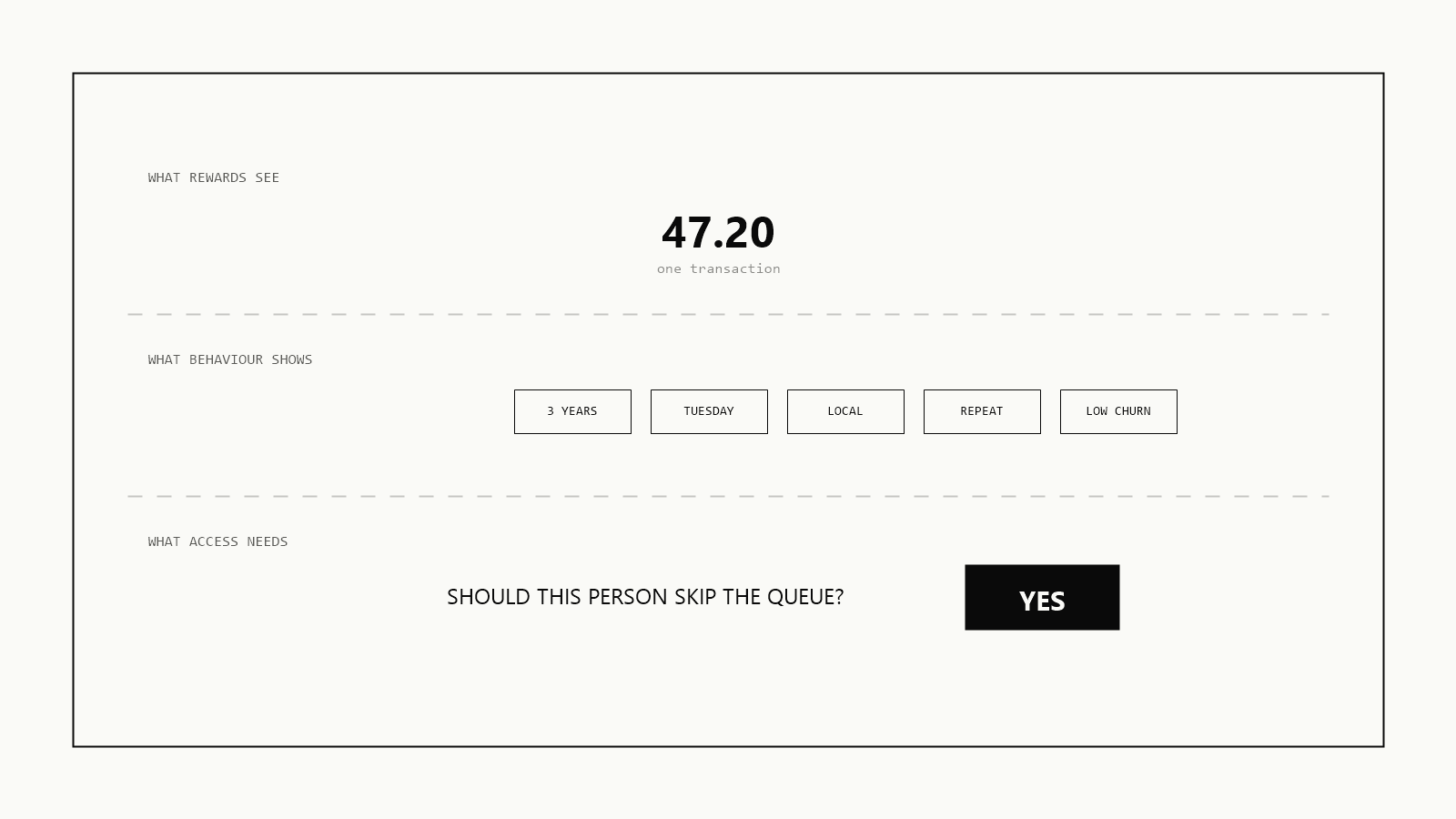

A receipt can say this person has:

- been a customer of independent cafes in this neighbourhood for three years.

- returned to this artist across multiple calendar years.

- completed marketplace transactions with no chargebacks across a multi-year window.

That information is commercially useful. It is also sensitive. That is why the shape matters.

The important part is what the receipt refuses to become. It is not a life score. It is not a public leaderboard. It is not a bank selling your entire behavioural graph to every merchant with a campaign budget. It is a narrow answer to a narrow question, provided by the person when the door is worth opening.

Enough proof for the door. Nothing extra.

That is the difference between a reward layer and a surveillance layer.

The door is different in every market

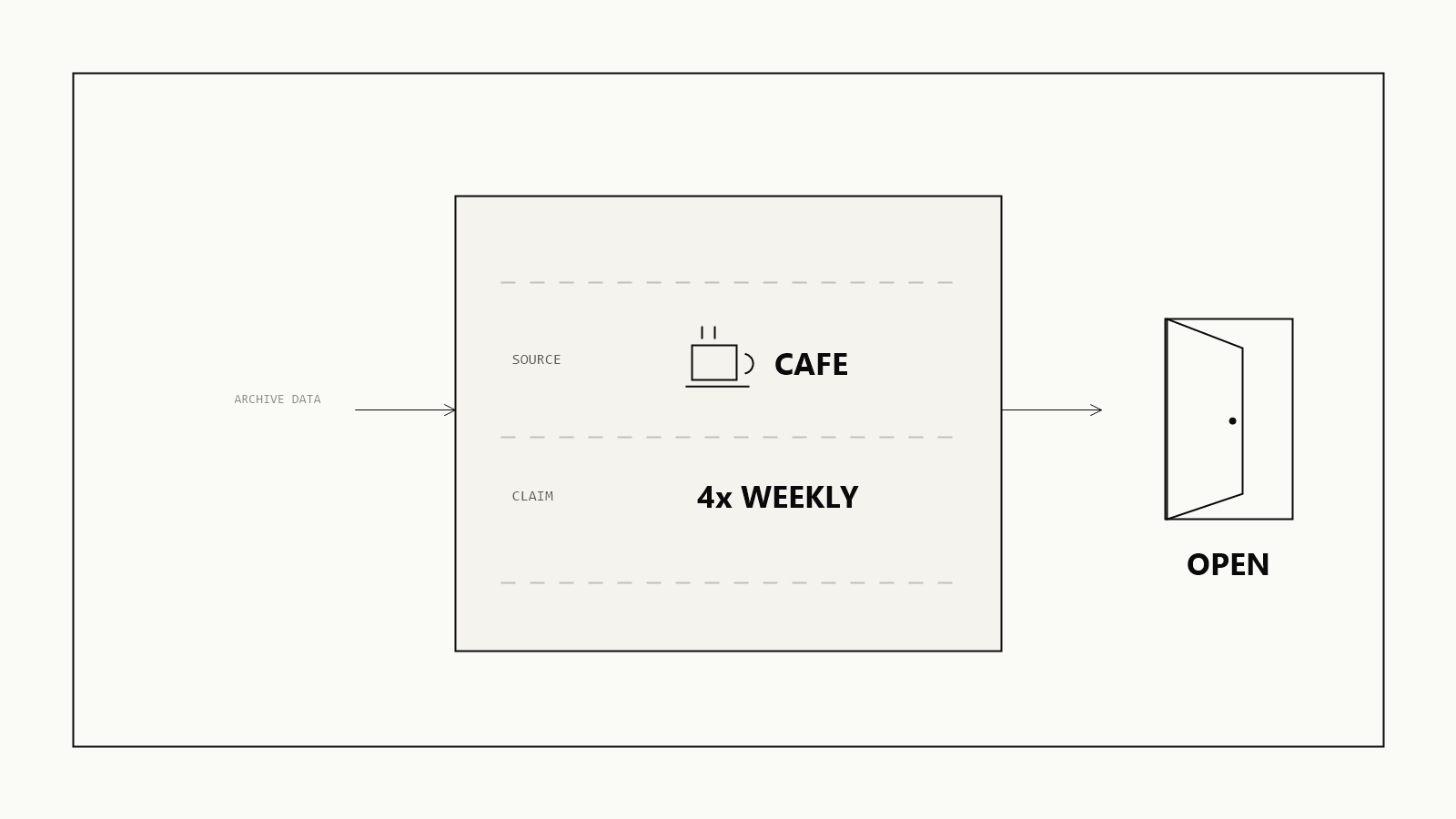

A new cafe does not need to spray discounts at everyone within five miles. It needs the fifty people whose spending pattern says they actually try new places, return to the good ones, and live close enough to matter. Give those people first right of refusal. Sell them a better-than-meh experience and you might find the first people who make the place work.

An artist does not need to reward the loudest fan on campaign week. They need to find the people whose behaviour predates the campaign, before the reward existed, before the signal was visible enough to perform. If someone has returned to an artist across seven years, they should not be fighting the presale queue on the same terms as someone who heard one song last Wednesday.

A marketplace does not need another generic trust badge. It needs to reduce friction for the users whose records show clean participation over time. Not a permanent score of the person. A specific proof for a specific moment.

That is not a cashback problem. It is a proof problem. And AI makes the proof problem more urgent.

The custody question decides the market

The custody question decides whether it becomes useful or creepy.

If the bank owns the archive and sells the read, the user risks becoming inventory. If the user holds the archive and lets a requester verify a narrow claim, the user becomes the routing point. The mechanism has to be a consented request, a narrow verification, and no export of the underlying graph. Same behavioural intelligence. Different power structure. Different market.

This is where Chris Dixon's Read Write Own is useful as a background frame, not as a detour. Applied to rewards, the useful ownership idea is simple: the user should be able to carry what they have earned out of one system and into another. The useful object is not the platform's private score. It is the user's portable proof.

That is where the more interesting version of loyalty is pointing.

Not "we might pay for your sandwich." Not "here is 2 percent cashback." Not "collect 9,000 points and redeem them for a disappointing voucher."

The better question is: what has this person already earned the right to access?

When claims are cheap

The timing matters because generative AI is making the surface layer cheaper. Profiles can be polished. Reviews can be generated. Claims can be written beautifully. Audiences can be inflated. Even loyalty can be performed once the reward is known.

What is harder to manufacture quickly is old, source-bound behaviour. Not impossible to fake. Harder. More expensive. More dependent on calendar time, recurrence, and provenance.

A mature reward layer should understand that difference. It should not treat every tap as a lottery ticket. It should not turn every person into a score. It should let behaviour become proof, and proof become access, without forcing the whole archive into public view.

The user keeps the record. The merchant gets the answer only when the user approves. The reward matches the behaviour. The value is shared. The feeling becomes mutual.

That is the version of loyalty worth building.

The card that might not charge you is a clever hook.

The deeper product is the layer that knows when you should not have to queue.